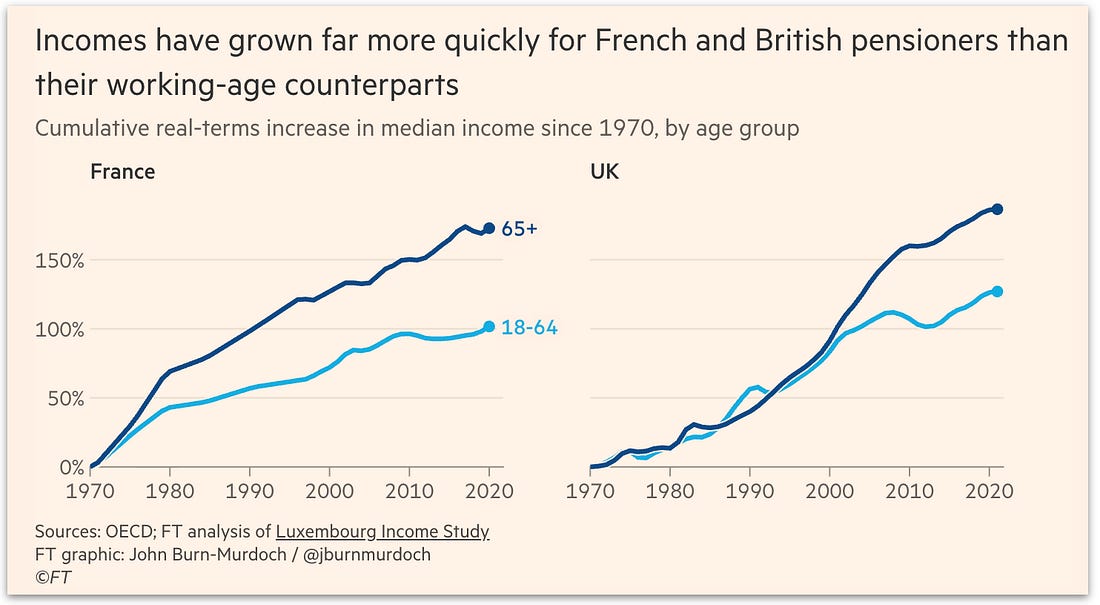

⁉️ The great value inversionWhy degrees depreciate, pensioners prosper, and private equity needs retail moneyHi all, this essay first appeared in my weekend note for Exponential View members three days ago. Here’s an excerpt – if you’d like to read the full piece, you can upgrade your membership for access. Has value broken? Stalwart signals are looking funky. Electricity trades at negative prices while grids collapse from surplus; university credentials lose worth as trade apprenticeships command premiums; private equity’s titans turn to retail money. Do these inversions reflect random noise, temporary disruptions in otherwise stable systems? Or are they symptoms of something more profound: a revaluation crisis that challenges how we price the future itself? Frankly, it’s a bit odd when abundance creates crisis and scarcity drives prosperity. Perhaps our fundamental economic grammar, the language of supply, demand, and equilibrium we’ve trusted since Adam Smith, is out of date.

Look at higher education. A new Gallup poll reveals that only 35% of Americans now view college as “very important,” down from 75% in 2010. Is this mere anti-intellectualism? Or a rational response to a labor market being hollowed out by precarious work, post-COVID fatigue, climate doomerism or automation? In the UK, PwC cut graduate recruitment by a third. The CEO of British placement agency Reed advises students to consider manual labour over degrees. Some may believe that the credential that once guaranteed middle-class stability – steady employment, home ownership, upward mobility – now delivers neither certainty nor wages sufficient to offset its cost.

These inversions extend deep into our financial markets. Private equity, once the apex of sophisticated capital allocation, has turned to courting retail investors to access their 401(k) accounts. Why? Because the industry needs fresh capital to sustain its model. Private equity cannot sell its companies; exits have crashed to two-year lows. This isn’t charity; it’s plumbing. With IPO windows grudging, M&A selective, and continuation funds propping up timeworn assets, managers are widening the intake pipe while the outflow remains tight. That is why the smartest money in the room needs the dumbest. The math no longer works: cheap debt has gone, but lofty valuations remain. Software is no longer eating the world. It is demanding a new world. Meanwhile, our energy system, built on the language of shortages, waste and efficiency, desperately needs a new vocabulary…

|

⁉️ The great value inversion

Wednesday, 24 September 2025

Subscribe to:

Post Comments (Atom)

No comments:

Post a Comment