This is Brad DeLong's Grasping Reality—my attempt to make myself, and all of you out there in SubStackLand, smarter by writing where I have Value Above Replacement and shutting up where I do not… Yes, Kevin Hassett Would Be a Very Bed Fed ChairLying liars who lie and knowingly and deliberately say whatever—whatever—lies they believe are to their immediate advantage are not the kind of people who should chair the Federal Reserve. Any...Lying liars who lie and knowingly and deliberately say whatever—whatever—lies they believe are to their immediate advantage are not the kind of people who should chair the Federal Reserve. Any questions?Time to fire up the WayBack machine and run the videotape. Why economists shake their heads and sigh when Kevin Hassett’s name is brought up, and talk about how great a waste of it all it is. Back before 2000, Kevin Hassett and James Glassman spent their days telling lies. Back then, they spent their days telling lies about what bog-standard present-value finance calculations said was then the "fundamental" value of the stock market. They claimed that:

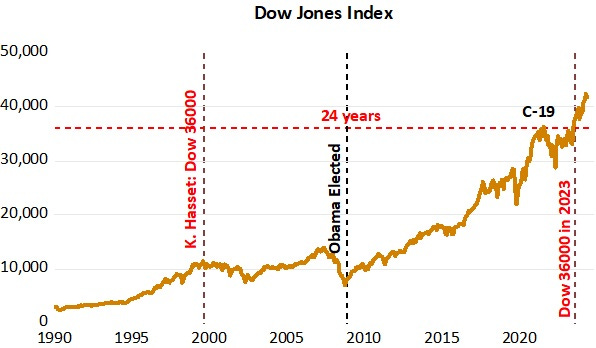

That was the title of their book: Dow 36,000: The New Strategy for Profiting from the Coming Rise in the Stock Market <https://www.amazon.com/Dow-36-000-Strategy-Profiting/dp/0609806998>. That was their claim: "our analysis justifies a Dow of about 36,000—not in five or 10 years, but right now." (Relative to inflation, a DJIA of 36000 in 1998 corresponds to 72000 today; relative to the size of the economy, A DJIA of 36000 in 1998 corresponds to 108000 today; relative to corporate profits, a DJIA of 36000 corresponds to 180000 today. The DJIA this AM is one quarter of that, just as the DJIA back in 1998 was 1/4 of what it was then. The Glassman-Hassett valuation claims were off by a factor of four then. Their methodology is still off by a factor of four now.) Of course it did not happen. If you had bought the Dow at 9000, and if you were forced by liquidity to sell at the trough over the next half-decade, you did not quadruple but instead lost 20% of your money. If you had been unlucky enough to buy at the peak and be forced by liquidity to sell at the trough, you lost 40%. When challenged by people who said that their math seemed, wrong, Glassman attempted a partial walk-back:

Which partial walk-back, of course, involved a big bold-faced lie. Glassman (and Hassett) had not claimed that the fundamental value of the Dow then at 9000 should be in the range of 13500 to 36000—“roughly 50 percent… higher… [to] 300 percent higher”. Glassman and Hassett had claimed that their fundamental analysis: “justifies a Dow of about 36,000--not in five or 10 years, but right now." Hassett, to my knowledge, did not at the time attempt even a partial walk-back when challenged. The extremely sharp Clive Crook <https://web.archive.org/web/19991231025452/http://www.slate.com/Dialogues/98-04-29/Dialogues.asp?iMsg=1> called Glassman and Hassett on this at the time:

Crook was and is entirely correct, except in one thing. That one thing? I know that in Hassett’s case it was not “because [he had] not understood [his] ‘simple finance formula’…” There is no “not understood”. Hassett understood and understands the Gordon fundamental-valuation finance equation very well. (Glassman, I am not so sure.) The “payouts” Gordon fundamental-valuation equation (a) takes current dividends as payouts and divides them by the difference between the required rate of return and the growth rate of dividends. If you want to use earnings rather than dividends, there is an alternative “resources” equation you can use (b) which takes earnings as resources and divides them by the required rate of return. Resources can either be paid out now, or used to produce growth and so higher profits that can be paid out in the future. Add the value of (a) current payouts to the value of (b) growth produced by investment, which is (c) the difference between resources and payouts. When you do that addition “payouts” cancel, and you are left with the value of resources. (And you then have to add on a term capturing the company’s ability, if it has one, to make investments with above-market returns.) Glassman and Hassett took the “resources” from (b) and pretended they were the “payouts} from (a). They thus double-counted retained and reinvested earnings both as a source of current cash flow and as a driver of profit growth. A given dollar of earnings can be either cash-flow paid out to investors or reinvested to drive profit growth, but not both. THIS IS NOT SUBJECT TO DEBATE. In Hassett’s case, at least, this is a deliberate, conscious, malevolent lie. Plus—plus!—to get to their Dow 36000 number then, they had to make the highly counterfactual assumption that the equity risk premium really ought to be not smaller but zero. And, to justify the prediction that the DJIA would go to 36000 over the next three to five years, that whatever factors had been causing the actually-existing risk premium were about to completely stop. Why did Glassman and Hassett tell these lies back then? Nobody could ever advance an explanation other than that they wanted to get noticed and sell books. And Hassett, at least, has not changed his MO in the past three decades. Here he is, still telling lies, today about the Bureau of Labor Statistics:

Back before 2000, I thought that Kevin Hassett had close to destroyed his career by showing that he was a person who was willing to tell bald-faced lies about his analysis, double-down when challenged, and then double-double-down again when challenged more, for no reason other than to sell books. I might have said some things to people who had been on the faculty of the University of Pennsylvania when Hassett went to graduate school there about unprofessional behavior of some of their Ph.D.’s, and how this might reflect some deficiencies in the “moral education” part of the curriculum. I might have said to Allan Meltzer that it was unprofessional of him to have given the book a blurb, even though Allan claimed that his “every stock owner should read this book” blurb had been intended as snark. (Which, I must say, they might have taken with very good graces.) But it did not matter for his career as a hewer of wood and a drawer of water for Republican politicans. Professional Republican politicians seem to have been attracted to an “economist” with a demonstrated reputation for being willing to say absolutely anything for some short-term benefit he perceived. Various Presidents and Boards of the American Enterprise Institute similarly had no problem with Hassett. He had a career. His willingness to say whatever he thought he was incentivized to say was a thing people on the other side of the aisle found very pleasing. Never mind that his elders and peers in academia would always shake their heads and sigh when his name came up. Never mind that in the circles in which I moved and move, the principal reaction to Hassett is a kind of pity—a waste of talent, and someone who cannot but look back at his life and see a life wasted. The general reaction seemed to be to judge Hassett more-or-less as Platon had his character Sokrates argue in the Politeia <https://www.perseus.tufts.edu/hopper/text?doc=Perseus%3Atext%3A1999.01.0168%3Abook%3D9%3Apage%3D577> that we should judge a tyrant: as a person who was actually in the condition of the most wretched slave. And we should lament the waste of it all. Why? Because for Kevin, as for the tyrant:

And if the mental imbalance of such a person is such that he does not recognized how pitiable his situation is? Then that only makes him more pitiable still, and it all even more of a waste. One is driven to give him the advice given by Dean Wurmer in Animal House: “that is no way to go though life, son…” And it would be really, really unfortunate for the country and the world were any senator to vote to confirm a Kevin Hassett as Fed Chair. If reading this gets you Value Above Replacement, then become a free subscriber to this newsletter. And forward it! And if your VAR from this newsletter is in the three digits or more each year, please become a paid subscriber! I am trying to make you readers—and myself—smarter. Please tell me if I succeed, or how I fail… #kevin-hassett |

![]()

![]()

No comments:

Post a Comment