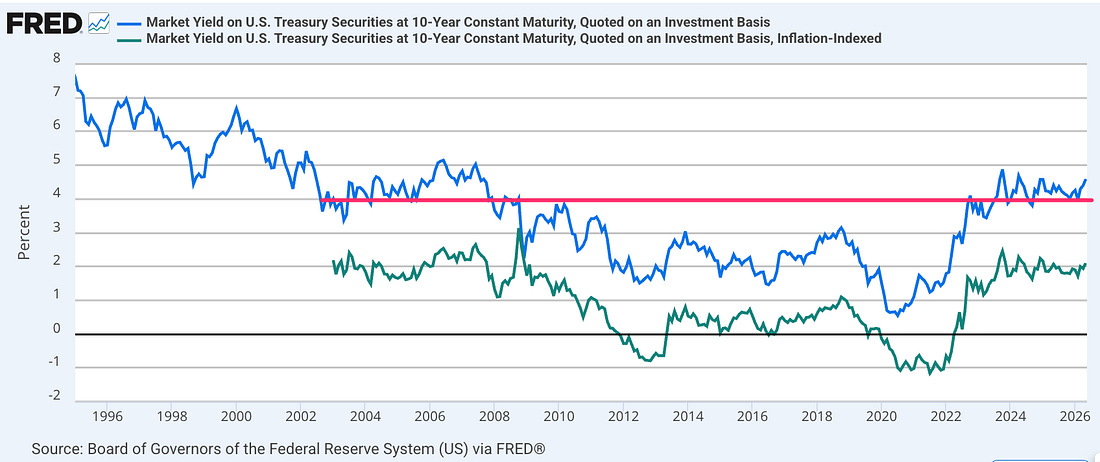

This is Brad DeLong's Grasping Reality—my attempt to make myself, and all of you out there in SubStackLand, smarter by writing where I have Value Above Replacement and shutting up where I do not… Bond market confidence that the Federal Reserve will be willing and able to keep inflation near its CPI-basis target of 2.5%/year has not yet cracked, at least not among those trading between long Treasuries and long Treasury Inflation-Protected Securities:

Yes, Kevin Warsh told people a lot of lies in his now-successful campaign to become Fed Chair. But the bond market is betting that the lies were the reassuring stories he told Donald Trump about how he would eagerly and aggressively cut interest rates as soon as he could convince his FOMC to do so. It is not clear to me that placing a 0% weight on the other possibility—that Kevin Warsh was lying to all those whom he and his affinity assured he would be a “normal” Fed Chair, and that he will do Donald Trump’s bidding, up to and including firing all the Fed Bank Presidents and appointing corrupt Trump shills in their places, and so transform the FOMC utterly—is justified. Why, you may ask, would Kevin Warsh do Trump’s bidding? For the same reason that since Paul Ryan decided in the summer of 2016 to go all in on trying to elect Donald Trump, nearly every Republican of note who formerly had a reputation has thrust themselves forward to do Trump’s bidding. Trump, you see, has since early 2016 had three superpowers:

And so ever since early 2016, the calculus of nearly all Republican worthies, save Mitt Romney, John McCain, and Jay Powell, has been that we avoid antagonizing Trump, because he could take us down now. And we also avoid playing any long game to remove him, because that would advantage the Democrats right now, and because his senility and stupidity will soon take him off of the game board anyway. Nevertheless, it is shocking and appalling that all 53 Republican senators and John Fetterman of Pennsylvania voted to confirm Kevin Warsh. Five of them should have been willing to say: We are sorry Kevin, but you have told too many lies—we are not sure to whom—to reach this point, and it is better to leave Jay Powell as Acting Chair, at least until the next session of Congress. Then, again, maybe Jay Powell told them that he intended to be, effectively, Acting Chair—to be primus inter pares on the Federal Reserve Board. And as long as he, Waller, Barr, Cook, and Jefferson hold phalanx, Warsh’s Trumpy Mr. Hyde self will only have the support of Michelle Bowman, she who blames illegal immigration for high housing prices. Indeed: Long-term U.S. Treasury interest rates not only suggest that inflation expectations are still well anchored, they also are still at levels low enough that the real borrowing cost to the government is lower than the rate of growth of the U.S. economy. That means that you can—if you set U.S. real GDP as your numéraire, which perhaps you should not, for lots of reasons—still see the U.S. government-budget constraint as not binding except in a left-tail scenario. The US national debt can still be viewed as a resource center for the government via the provision of collateralizable safe-asset services, rather than as a burden. It i true that we are not still in the world of “secular stagnation” or of the “global safe-asset shortage”. But we are still in the post-2001 world of what Ben Bernanke back then called the “global savings glut”. And we are definitely not back to the 1993 world in which the level and trajectory of the debt was a dire economic emergency. Interesting times, indeed. If reading this gets you Value Above Replacement, then become a free subscriber to this newsletter. And forward it! And if your VAR from this newsletter is in the three digits or more each year, please become a paid subscriber! I am trying to make you readers—and myself—smarter. Please tell me if I succeed, or how I fail…##back-to-the-days-of-the-global-savings-glut-chart-of-the-day

|

|

||||||||||

![]()

![]()

No comments:

Post a Comment